All agents have to complete real estate continuing education, but the best don't stop there. Our industry is ever-changing, and the most successful agents are the ones who never stop learning.

That’s why we’ve put together this collection of deep-dive resources just for you. These resources go beyond what's covered in our Real Estate Finance and Closings CE course, giving you deeper insights, fresh perspectives, and actionable strategies to apply in your day-to-day business. So dive into these expert-approved reads and keep pushing your business forward.

1️⃣ Winning at Underwriting

Even well-qualified buyers can stumble in underwriting, but this guide lays out how to keep loans on track. It reveals the top reasons mortgages get denied and how to prevent them – from credit score rehab to managing debt. You’ll learn why a solid preapproval isn’t bulletproof and what not to do before closing (hint: don’t go buying a new car!).

The advice is refreshingly actionable: for example, check and boost credit scores before applying and caution buyers against any moves that could jeopardize their approval. Arm yourself with these tips and you’ll save your clients from last-minute loan nightmares – a huge win for your reputation.

2️⃣ Know Before You Owe: TRID

The TILA-RESPA Integrated Disclosure (TRID) rules shook up the closing process with new Loan Estimate and Closing Disclosure forms, replacing the old HUD-1. Staying current on TRID is crucial, and this update from the Richmond Association of REALTORS® breaks it down in plain English.

It even brings good news for agents: Regulators realized it’s “usual, accepted, and appropriate” for lenders to share the new Closing Disclosure with real estate brokers. In other words, you can finally get the closing info you need to guide your clients, without the old privacy roadblocks.

This quick read will get you up to speed on the latest TRID tweaks so you’re never left in the dark at the closing table.

3️⃣ Roller-Coaster Rates: Market Trends

Wondering what’s up with today’s crazy market? This CoreLogic year-end report reads like a story of 2024’s wild housing ride. It spotlights how interest rates shot to unexpected heights, slamming affordability to the lowest levels in decades and sidelining many buyers.

At the same time, it notes a new wave of creativity – buyers teaming up and finding novel ways to finance homes when traditional routes got tough. The narrative is engaging and data-backed, giving you talking points on everything from rising rates to resilient buyer strategies.

It’s a must-read to sound like a market expert with your clients, and to anticipate how these trends could affect the deals you’re working on right now.

4️⃣ Insider’s Guide to FHA and VA Loans

Government-backed loans can be game-changers for your clients, and this explainer makes it easy to see why. It breaks down FHA loans – which offer lenient credit requirements and down payments as low as 3.5% – versus VA loans, which are a fantastic zero-down benefit for our veterans.

You’ll discover that VA loans are often easier to qualify for than conventional mortgages and usually require no down payment at all. The article highlights the quirks of each program (like FHA loan limits and the VA’s certificate of eligibility) in a clear, digestible way.

After reading, you’ll be better equipped to match buyers with the right loan and tout the advantages of these programs – a great way to add value as their agent.

5️⃣ How to Prevent Deal Disasters

Every agent has a horror story about a closing that almost fell apart. This Bankrate piece prepares you for those moments by listing the five most common closing delays and how to avoid them. Financing issues top the list – rising interest rates have blindsided some pre-approved buyers and diminished their buying power.

Low appraisals come next (did you know 21% of delayed contracts are due to appraisal gaps?!), followed by inspection surprises and title hiccups. The tone is upbeat and solution-oriented, suggesting steps like staying in close contact with lenders, prepping clients for potential appraisal shortfalls, and double-checking title reports early.

Read this and you’ll walk into every closing with eyes wide open and a game plan to keep things on track.

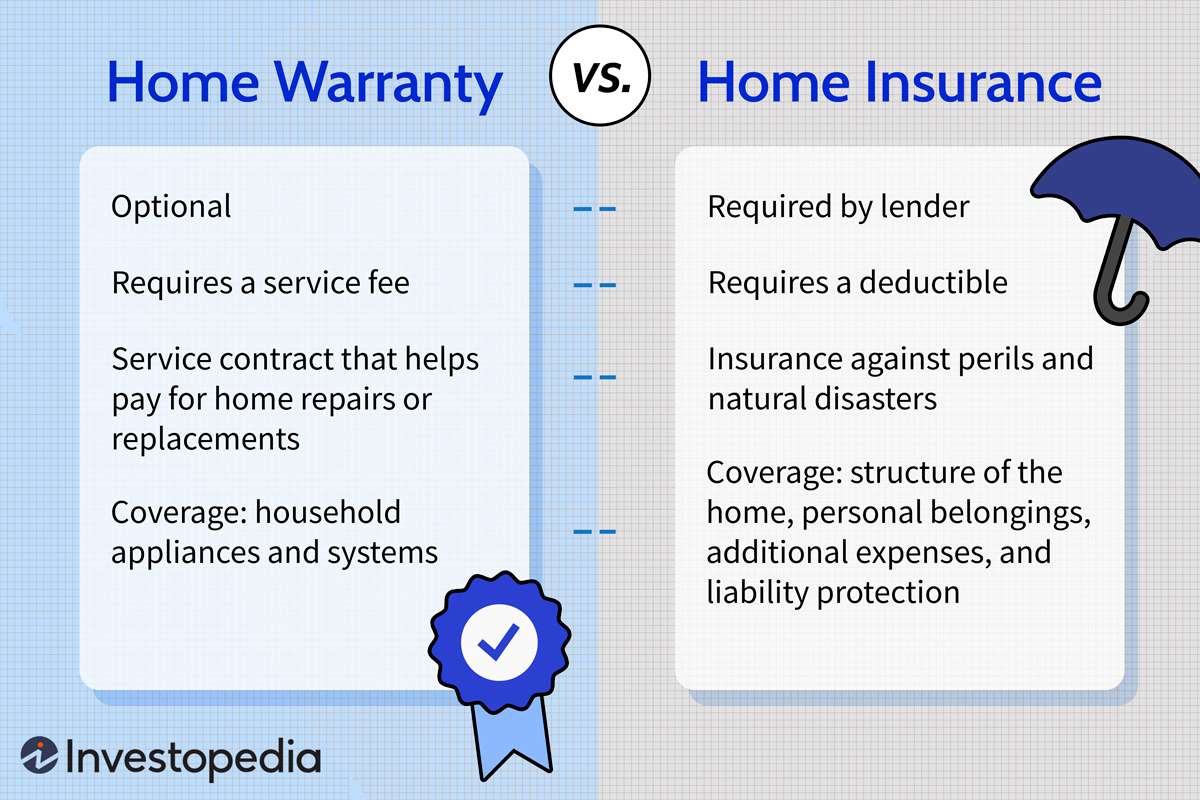

6️⃣ Insurance vs. Home Warranty

Homeowners insurance and home warranties both protect your buyer’s new home, but they’re not the same thing. This friendly guide highlights the differences so you can advise your clients with confidence. In short, a home warranty is a service plan that covers repairs/replacements for appliances and systems (think HVAC, plumbing) when they break from normal wear and tear.

Homeowners insurance, on the other hand, guards against big perils like fire, storms, or theft – and even provides liability coverage if someone gets hurt on the property.

The article points out that insurance is usually required by lenders, whereas a warranty is optional but can offer extra peace of mind. Share these insights with your buyers so they don’t confuse the two, and help them decide if adding a home warranty is worth it for their situation.

7️⃣ Hidden Home Hazards

Homes can harbor secrets, and this eye-opening read from McKissock (a real estate education source) will help you spot them. It runs down common environmental hazards lurking in houses. Some are old news – like asbestos, which was used in everything from insulation to siding until it was finally banned in 2024 – and some might surprise you.

Ever heard of “Chinese drywall”? Homes built in the early 2000s sometimes used imported drywall that emits smelly sulfur gases, causing health issues and corroding metal in the home. The article also covers mold, lead paint (still found in pre-1978 homes), and more. It’s written in an engaging way, so you don’t need a science degree to understand it.

By reading this, you’ll pick up tips to recognize red flags and ensure your buyers aren’t walking into a health hazard. Knowledge is power – and in this case, it could also be a lifesaver.

8️⃣ Assumable Mortgage Magic

This true case study reads like a victory lap for creative financing. A Bankrate writer shares how she struggled to sell her home – until her agent highlighted an assumable FHA loan attached to the property. An assumable mortgage lets a buyer take over the seller’s loan at the existing ultra-low rate (in this story, just 3.875%).

That became the home’s biggest selling point in a high-rate market. The article walks you through the process (it’s a bit complex, but doable with teamwork and the lender’s OK) and the outcome: The home, marketed with that sweet low-rate loan, sold within a month at full price!

The author gives credit to her savvy real estate agent for suggesting this strategy and coordinating the details. It’s an inspiring read that might spark ideas on how you can save a deal or attract more buyers by leveraging an assumable loan or other creative financing tools.